Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

August 14, 2022 at 02:36 PM

August 14, 2022 at 02:36 PM

What You Need to Know

- Monthly home value declines have now engulfed 22 of the 100 largest metropolitan areas, though inventory is still very tight.

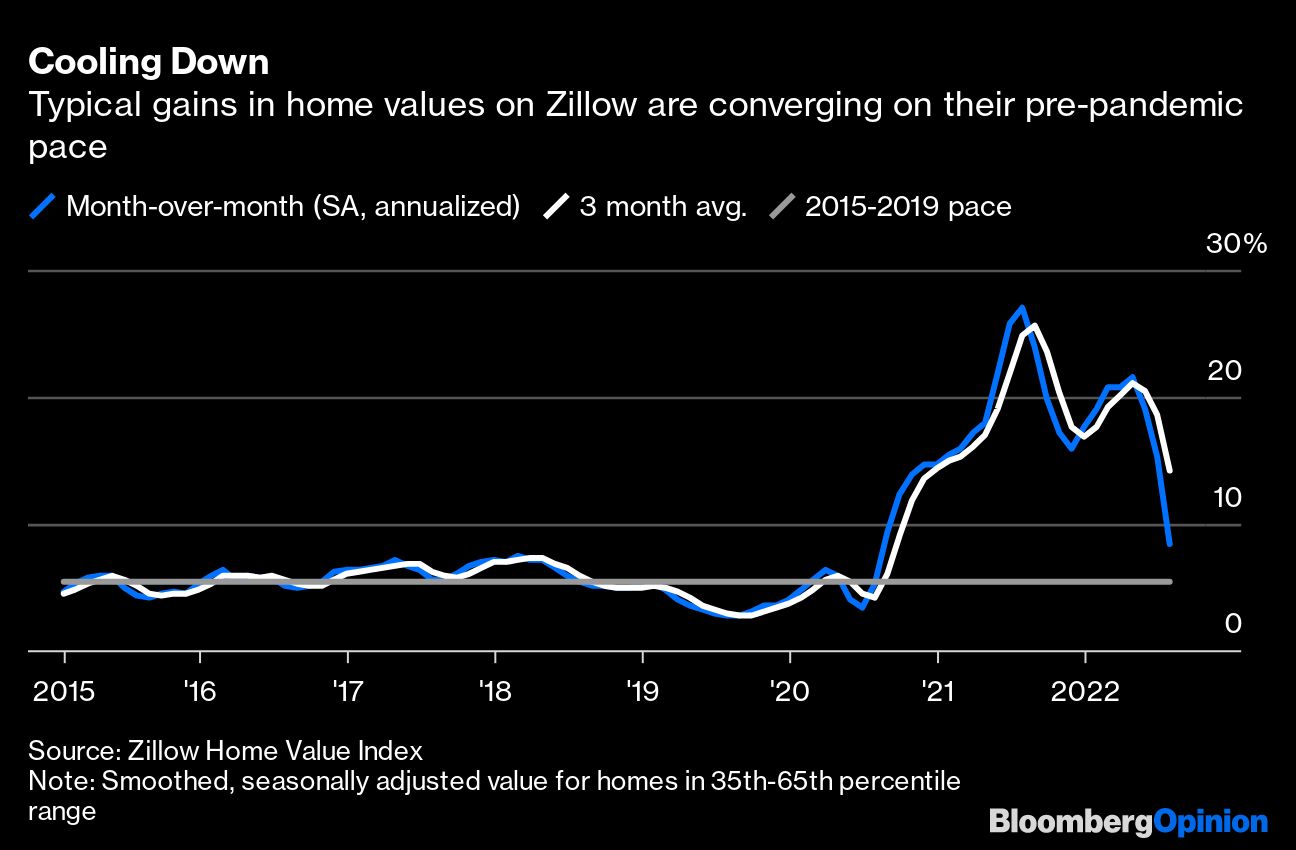

Home price appreciation is slowing fast across the country under the weight of higher mortgage rates, with typical property values even falling month-over-month in about a fifth of major metro areas in July.

Clearly, the slowdown is necessary if Federal Reserve policy makers are going to cool inflation and restore affordability to the housing market. The challenge is to prevent the deceleration from becoming a collapse, but monetary policy makers have a chance to pull it off, provided unpredictable outside forces cooperate.

Nationally, typical home values rose a seasonally adjusted 0.7% last month from June, according to the Zillow Home Value Index data released Friday. That’s consistent with 8.5% home value appreciation on an annualized basis, a considerable downshift from a pace of around 25% in mid-2021.

The Fed is coming in hard and fast on the 5% pace that was common in the five years before the pandemic, which would finally be consistent with its goal of bringing inflation back under control.

But will the market stop on a dime when it hits that 5% pace, or at least avoid going negative?

Ultimately, that all depends on the evolution of inflation broadly; the Fed’s determination to push interest rates higher; and whether policy makers end up driving up unemployment in the process. The odds of a positive outcome look marginally better in the light of recent data.

Home prices aren’t directly part of the inflation index because housing is considered an investment instead of a consumer good. Instead, the main U.S. inflation indexes track a concept called owners’ equivalent rent, which is supposed to capture the cost homeowners would incur if they had to rent back their homes.

As a consequence of the quirky methodology, shelter inflation is closely correlated with housing market metrics, but it tends to lag market prices by many months.

The U.S. received encouraging news on Wednesday when the consumer price index showed tentative signs of easing inflationary pressures. Core prices — which exclude volatile food and energy — rose just 0.3% month over month, a 3.8% annualized pace.