Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

July 15, 2021 at 05:14 PM

July 15, 2021 at 05:14 PM

What You Need to Know

- Biden's plan to impose payroll taxes on high earners would create a gap between earnings above $400,000 and those at $142,800 or less.

- High-earning clients might be able to offset, defer or reclassify income to avoid the extra tax.

- While there has been little talk about this plan lately, lawmakers are well aware that the Social Security and Medicare trust funds have shortfalls that need to be addressed.

If you stroll through the streets of Chicago, you have likely heard from the locals and longtime transplants about the famous Stan’s Donuts & Coffee on North Damen Avenue. Though skeptical and deviant from my preferred desserts, I must profess — the donuts live up to their hype.

Yet there is another, far less savory donut — or at least a donut hole — that has everyone talking: President Joe Biden’s plan to impose payroll taxes on earnings above $400,000, creating a “hole” between that figure and the current ceiling of $142,800 in taxed wages.

Payroll Tax Rates

For wage earners, Social Security and Medicare taxes — collectively known as payroll taxes — equal 6.2% and 1.45%, respectively, and are automatically withheld from paychecks by employers under the “pay as you go” tax system. Note that for 2021, Social Security taxes are only applied up to $142,800 in earnings, but Medicare taxes have no income limitation.

In addition, there is an “additional Medicare tax” of 0.9% that applies to earnings exceeding $200,000 (single) and $250,000 (married filing jointly) of adjusted gross income (AGI). Except for the Additional Medicare Tax, employers pay an equivalent share of these taxes on the wage earners’ income but can deduct these taxes on their tax returns.

Meanwhile, self-employed individuals, who act as both an employer and employee, are responsible for paying both shares of these taxes through quarterly payments. Referred to as self-employment taxes, the Social Security tax equals 12.4% of up to $142,800 in 2021 earnings, while the Medicare portion equals 2.9% without limit.

Self-employed individuals also face the Additional Medicare Tax, but the rate stays at 0.9% since it only applies to the employee portion of earnings. Lastly, and not including the Additional Medicare Tax, self-employed persons can deduct the employer portion of self-employment taxes as an adjustment for AGI.

The Donut Hole

Payroll taxes are an important piece of government revenue collection and are used to fund federal insurance programs such as Social Security and Medicare. In fact, in 2019, payroll taxes accounted for 38% of Internal Revenue collections; second only to income taxes at 57%.

In recent years there has been much concern regarding the solvency of these programs, especially Social Security. The 2020 Annual Social Security and Medicare Trust Fund Report estimates that full benefit payments can be paid until 2034, when payments would decrease to 79% of benefits.

Social Security has faced solvency issues before, only to be later resolved through tax reforms. Perhaps most noticeable were the 1983 amendments to the Social Security Act. However, reform takes many faces, and who it ultimately impacts depends on current lawmakers and public perception.

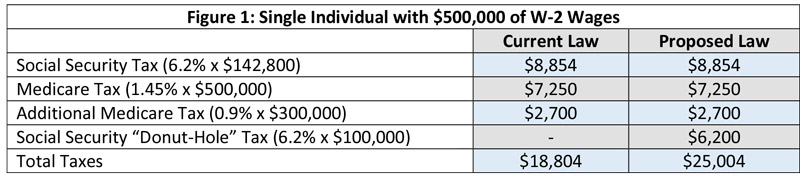

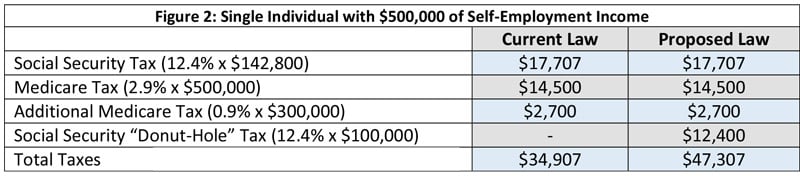

Biden’s proposal for reform is reimposing the Social Security tax on employees and self-employed persons earning over $400,000, thus creating a donut-hole effect from $142,800 to $400,000 in earnings.

Medicare taxes, however, would remain unchanged. Figures 1 and 2 demonstrate the severity of these proposed changes. In both scenarios, the taxpayers roughly face a whopping 33% tax increase!

Implications

It should be noted that few taxpayers would be affected by the payroll tax increase because only 1.8% of households exceed $400,000 of total income. In addition, even if a household exceeds that number, there is likely a strong chance that some (or much) of that income is from other sources like passive or portfolio income, which are not subject to payroll taxes.

Lastly, Social Security is a social insurance program that is designed to favor neither the rich nor poor. This is roughly accomplished in two ways.

First, the Social Security Administration uses actuarial calculations to help ensure that cumulative retirement benefits are approximately equal to lifetime contributions regardless of whether a recipient starts benefits early or late at reduced or enhanced levels, respectively.

More specifically, benefits are based on an individual’s highest 35 years of inflation-adjusted earnings. Upon the full retirement age (FRA), which is either age 66 or 67 depending on birth year, retirees can claim their full unreduced benefits.

Conversely, retirees can claim benefits as early as age 62, but with a 25% reduction, or claim as late as age 70 with a 24-32% increase. This is important because wealthier retirees typically can afford to delay Social Security, thus enjoying enhanced benefits, whereas less wealthy retirees may need to claim early to supplement retirement income needs and consequently face permanently reduced benefits.

Second, despite Social Security taxes being regressive because of their fixed percentage and taxable earnings ceiling, subsequent benefits are progressive because lower earners receive higher replacement ratios on lifetime contributions.

In addition, in 2021 the maximum individual benefit at full retirement age is $3,113 per month, thus higher earners cannot receive outwardly disproportional benefits. Altogether, Social Security is more impactful on a lower earning individual in retirement.

What remains unclear, however, is if Biden’s proposal would include a secondary earnings limit and subsequently larger Social Security benefits to help offset the additional upfront taxes. If not, higher earners falling on the wrong side of the donut hole may now be faced with what is essentially an outright tax, without limitation, that acts as a subsidization tool for other Social Security recipients.