Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

By

By  August 20, 2020 at 02:05 PM

August 20, 2020 at 02:05 PM

For analysts at S&P Global Ratings, the possible effects of changes in life insurers’ interest rate assumptions is one of the question marks looming over the industry.

Deep Banerjee, a lead analyst at S&P, talked about his company sees life insurers Wednesday, during a web meeting S&P organized to review insurers’ second-quarter financial reports.

Three big, publicly traded have already slashed the interest rate assumptions they use to run their businesses.

“We expect more to follow suit,” Banerjee said.

(Related: 5 Things to Know About Life Insurers’ Investment Machinery, for Agents)

Interest rate assumptions matter to life insurers partly because the reserves they hold, and invest, to support long-term life, disability insurance, long-term care insurance (LTCI) and annuity obligations are enormous relative to the size of their net income.

Even small changes in rate assumptions may require them to top off reserves. Shifts of cash into reserves that are small relative to the size of the reserves may look huge relative to the size of an insurer’s typical earnings.

(Related: Unum Could Add Up to $750 Million to LTCI Reserves)

The lower the interest rate assumptions, the higher prices for new life, annuity, disability and LTCI products are likely to be, and the skimpier the benefits guarantees are likely to be.

Bondholders’ Pay Cut

From S&P analysts’ perspective, the big, publicly traded U.S. life insurers look as if they’re getting a manageable number of COVID-19-related life insurance claims, with claim costs well below stress-test levels.

For now, at least, life insurers’ portfolios of corporate bonds, mortgages and mortgage-backed securities look fine.

Banerjee emphasized that, overall, the life insurers S&P rates have been doing well, and in line with the insurers’ own predictions.

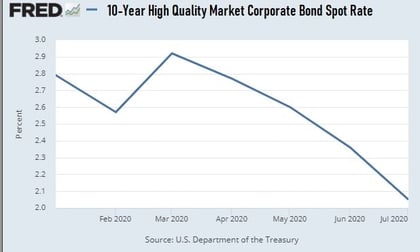

But life insurers hold trillions of dollars in high-quality corporate bonds, Moody’s Seasoned AAA Corporate Bond Yield chart shows that the yield available from the very highest rated corporate bonds has dropped to 2.3%. That’s down from 3% at the started of the year, and down from a level over 3.6% for most of the past five years.

S&P’s own S&P 500 10+ Year Investment Grade Corporate Bond Index shows that the average yield to maturity for the basket of high-quality corporate bonds it tracks stood at 2.93% Wednesday. That was down from about 3.6% a year ago.