Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

August 12, 2020 at 05:12 PM

August 12, 2020 at 05:12 PM

For advisors, model portfolios free up time to focus on comprehensive financial planning, estate and tax strategies, client relationships and client prospecting without giving up total portfolio control. But how do they choose the right ones?

In a recently released report, Morningstar lays out the pros and cons of model portfolios, which are growing at an accelerated rate; the universe of funds from which to choose; and some of their shortcomings.

About 400 model portfolios have been launched since the beginning of 2018, according to the report.

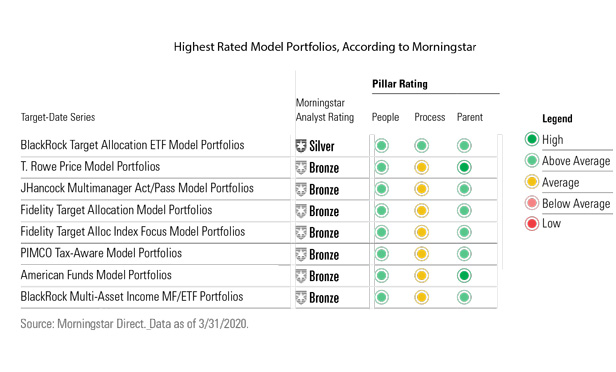

“If I were an advisor looking at model portfolios I would be looking at the people managing the portfolios and the resources supporting the asset allocation process … the proven records of success of the managers of the underlying funds, the sub-asset class allocations and how firms came up with those,” said Morningstar analyst Bobby Blue, one of four authors of the Morningstar report, 2020 Model Portfolio Landscape.

The “value add of model portfolios (or lack thereof) will hinge on the advisor’s due diligence process and implementation of the model,” according to the report, whose authors also include strategist Jason Kephart and associate analysts Adam Millson and Megan Pacholok.

Here are some of the basics of model portfolios that advisors should keep in mind, according to the Morningstar report. On the plus side:

- Model portfolios can be significantly cheaper than comparable mutual funds, especially actively managed funds. “Low costs remain one of the most appealing features of model portfolios,” according to Morningstar.

- They allow tax-loss harvesting at the individual client level, which isn’t possible in a multi-asset mutual fund

- Their holdings can be adjusted for client preferences of the underlying holdings, rebalancing and implementing tactical deviations from a strategic asset allocation

- They allow advisors to retain discretion over the asset allocation, underlying holdings, rebalancing frequency and trading.

On the negative side:

- Their proliferation has led to many models that are unproven

- Most have hypothetical track records that aren’t held to the same standard as other investment vehicles, which are regulated by agencies like the Securities and Exchange Commission or Labor Department (but about 25% have track records tied to another company vehicle such as a separate account or mutual fund)

- Changes to recommended underlying funds can introduce unintended risks (but such changes are at the discretion of the advisor)

Morningstar analyzed 563 model portfolios, after excluding about half the 1,100 models in its database that had reported a portfolio within the past six months.Their average expense ratios ranged from about 0.40% to 1.25%, with higher fees usually associated with greater equity allocation.

The Universe of Model Portfolios

More model portfolios use low-cost passive ETFs than actively managed mutual funds. The use of passive ETFs, along with no-fee ETF trades from such brokerages as Fidelity and Schwab, help to constrain costs, according to Morningstar. Vanguard and Charles Schwab model portfolios have an average asset-weighted cost of 0.06%, according to Morningstar, less than half of State Street’s 0.13% average and just one-fifth of iShares’ 0.30% average. “Firms that have low-cost philosophies also have the cheapest model portfolios,” according to the report.

Model portfolios using actively managed mutual funds, such as those from T. Rowe Price and John Hancock, have higher expense ratios ranging from about 0.40% to 0.90%. There are also many blended portfolios that combine passive and active funds. Generally the larger the equity allocation, the higher the expenses.

“A lot of active fund shops see model portfolios as a way to drive assets to their active products,” Blue said.