Four years ago, in December 2013, I highlighted Atlas’ seed-led venture creation model by walking through our Fund IX Seed Class of 2013. Only a short 1400 days ago, reading it again last week made it seem like an eternity. In the spirit of transparency around the mystery of venture fund portfolio construction, here’s a scorecard on the evolution of that Fund IX portfolio.

Seed-led investing remains a core part of our strategy. As described in that 2013 post, and true today, this is the essence:

Our seed strategy takes nascent substrate around new drug discovery platforms or therapeutic assets and incrementally but materially derisks them before committing significant capital and reserves. This derisking process is a “search for signal” – what can we glean about the underlying science/technology/asset, the founding team, and the market’s responsiveness to the concept that gives us the confidence to press forward. That search can involve conducting confirmatory experiments around reproducibility, completing early screens to judge the quality of the starting chemical matter, recruiting a great group of founders/entrepreneurs, or identifying a corporate partner…

Seed-led investing has a few practical and general points worth highlighting. First, “seeds” in our definition can either be standalone “rounds” or they can be initial “seed” tranches of bigger Series A rounds. Second, whatever the investment structure, the initial check sizes are small, typically less than $2-5M in total. Back in 2013, we often syndicated those seeds; today we tend to do them ourselves (more later). Third, they almost always involve co-founding a new startup that works closely with us during an incubation phase in our offices – the venture creation process. Lastly, during the seed stage the startups work against specific milestones, achievement of which will catalyze their graduation from the “seed pool” into the broader Atlas portfolio. Well-known graduates in the past include companies like Nimbus, Padlock, Delinia, and IFM.

As further background on Fund IX, our 2013 vehicle, the biotech portion of that $265M fund ended up investing in 19 new startups, so seven more than the initial portfolio revealed in the 2013 blog post. The vast majority (95%) were structured as standalone seed investments or as first tranches of Series A rounds with less than $3M from Atlas. The vast majority were co-founded by Atlas and incubated within our offices. This is the essence of Atlas’ venture creation model: co-founding, seeding, and incubating high impact, high risk therapeutics startups.

Portfolio Evolution

Here’s the summary of the portfolio’s progress since its debut in 2013, initially with an emphasis on the “constructive” learnings.

Four of the initial 2013 seeds were terminated during the seed process:

- Ascelegen: failed to robustly replicate biology around a novel growth factor for cardiovascular diseases, including heart failure.

- Lucena: failed to replicate pharmacology around modulation of a specific ion channel in Th17 differentiation.

- Project IO: failed to secure the rights to an academic T-cell therapy in the immuno-oncology space

- Project Thew: failed to identify a therapeutic path forward around emerging muscle regeneration biology (a Fund VIII deal).

Three more seeds initially transitioned into small Series A commitments before we either shutdown the deals or they changed direction with alternative business models:

- Raze: although it made intriguing progress, the underlying cancer metabolism biology was too complicated to warrant further investment; assets went back into academia for further exploration

- Quartet: their once-promising neuropathic pain program hit an unmitigatable preclinical safety issue in August 2017, detailed here, that led to the recent shutdown of the company

- Numerate: this one is not a failure at all, as this cool artificial intelligence-led drug discovery software startup continues to deliver. But they’ve done so with a different, more service/collaboration business model than our drug discovery platform thesis (so Atlas went passive).

The other 13 investments in the biotech Fund IX portfolio continue to mature nicely and are worth highlighting briefly: several companies were bought or are in the process thereof, three are now public, and six are actively tracking with stellar trajectories.

M&A: We’ve had multiple positive acquisitions or partial realizations through strategic deals: Padlock Therapeutics, focused on a novel autoimmune mechanism, was acquired by BMS in March 2016 (here); LTI, advancing a novel Parkinson’s program, secured an option-to-buy deal with Allergan in January 2017 that included a partial realization (here); and Harbor Antibodies was acquired by a Chinese-backed entity in December 2016. CoStim was another 2013 investment mentioned in my December 2013 blog post; although in Fund VIII rather than Fund IX, it was acquired by Novartis in early 2014 (here).

Public offerings: Several companies in the portfolio have now become publicly-traded entities: Intellia, our gene editing play, was seeded back in May 2014, went public in May 2016 (here); Spero, focused on novel antibiotics, was seeded in April 2014 and went public in October 2017; and Synlogic, advancing its engineered microbes for a variety of diseases, completed a reverse merger into Mirna in August 2017.

Active private portfolio: Seven companies remain active, private companies with great potential: Cadent is focused on allosteric ion channel modulators in the brain (and was formed via the merger of two Fund IX neuroscience companies, Ataxion and Luc); Navitor has developed mTORC1-targeted therapeutics for resistant depression, among others; Rodin is moving into the clinic in 2018 with its epigenetics-driven synaptic resilience program for Alzheimer’s and other dementias; Surface Oncology is transitioning into the clinic in 2018 with its novel immuno-oncology antibody portfolio; and Unum is progressing nicely in the clinic with its engineered Antibody-Coupled T-cell Receptor platform. Lastly, kDAC continues to explore the role of HDAC3 in oncology as an I/O potentiator, after unexpectedly failing to replicate the original academic data around HDAC3 in metabolism. Many of these emerging companies are making plans for accessing the public capital markets or entering into strategic deals over the next 12-24 months.

In sum, Fund IX’s biotech portfolio looks solid, and will almost certainly be a top decile venture capital vintage when benchmarked against the industry. It has benefited greatly from the seed-led venture creation model used to construct it. The derisking element of the seed process helps to bend the risk curve: take more of your losses on smaller amounts of capital, while powering up or transacting the therapeutic stories that are delivering.

This differential capital allocation between wins and losses is at the heart of the seed-led model in biotech investing, and the data from Fund IX support this concept. Our losses have taken an average of less than $2M in capital from Atlas, while our realized and unrealized “winners” have an average closer to 5x more than that. In four more years, when this portfolio is further matured, I’d be wonderfully surprised if we didn’t have some losses on larger, more long-in-the-tooth deals – but to date we’ve been fortunate to take most of the biological risk out of the equation on short dollars.

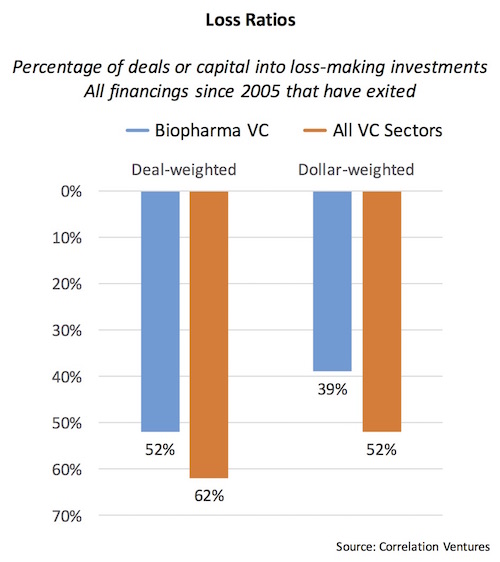

This bending of the risk curve has led to a very attractive overall loss ratio for Fund IX. While the deal-weighted loss ratio is around 30% today, the capital-weighted loss ratio is only 10% – which compares very favorably to the venture industry as a whole (52%) and biotech historically (39%), as described here.

{kind=link}

Reflecting on the construction of Fund IX, a few axioms of early stage venture investing are worth remembering.

Don’t power up the story until the early biologic risk is wrung out. The inability to replicate, extend, and generalize the underlying biological observations of academic findings continues to be one of the major reasons for early biotech failures. Pouring lots of capital in early can be a mistake in many cases. Even if you envision a broad platform company, reproducing the “exemplary case” for the platform – that foundational premise – is often well worth the time and energy spent in the seed phase. Since early stage biotech is almost always a bet on biology, derisking some of the biological risk early is of high value.

Truth-seeking behaviors are a blessing for quick, capital efficient kills in a portfolio. Although painful, the fail-fast/fail-early mantra is incredibly important, and surrounding startups with truth-seeking R&D veterans is helpful in driving it. The recent eulogy of Quartet Medicine, a failed investment, was a great example of this concept. The discipline of walking from investments that trend negative is key to the success of a seed-led investing model. A big part of this concept is creating the right entrepreneurial culture – which involves “recycling” talent into new opportunities. Of the six investments above that were shutdown, nearly every entrepreneur moved into another Atlas startup (e.g., Ascelegen’s EIRs helped start Intellia; Lucena’s CSO went into IFM; Raze’s head of biology helped found Obsidian and its head of chemistry co-founded Kymera, etc…).

Ownership only goes down over time with dilutive syndication. At the venture portfolio level, average ownership at exit is a major driver of fund returns (as described here in the Venture Math Problem). So if you over-syndicate your seed investments, you can’t recover the lost “ownership” in later rounds. We made that “mistake” in a number of our Fund IX deals (3- or 4-handed seed rounds), preventing us from owning a more significant portion of deals – especially frustrating for deals we co-founded and/or incubated in our offices. Giving away large pieces of the cap table early is as painful for seed-stage investors like Atlas as it is for founding entrepreneurs.

Our 2015 vehicle, Fund X, has been deployed with largely the same seed-led strategy and the early signals are incredibly positive. While we remain believers in syndication in Series A’s and beyond, we’ve addressed the early over-syndication issue, where most of our Fund X seed-stage investments have been principally only Atlas. We’ve already killed two seeds, and had two early fund-returning wins (Delinia and IFM). We’ve got a significant number of future value drivers, including AvroBio, Disarm, Kymera, Gemini, Magenta, Replimune, and many others – including a number of pre-launch stealth-stage startups that will be unveiled soon. Will be interesting to see where that fund goes in another 1400 days.